Hi Team,

Our Treasurer delivered what we expected last week, a cash splash into the NDIS, extra childcare support and more spaces allocated to provide guarantees so that some first home buyers can buy a home with a 5% deposit and single parents with only 2%. About time they got a break!

The only issue is the 10,000 spots will get chewed up in no time. People need to firstly get approved under the scheme and then very quickly find a place! We found that many missed out last year, so let’s hope it gets extended.

The company tax rate will continue to drop to 25% but this is a bit of a smoke screen for most small businesses. Owners still need to pay top-up-tax, up to their marginal tax rate, to get the profits out of their company to buy property and grow wealth in their personal names.

What’s more important is the extension of the Instant Asset Write off Scheme which allows immediate tax deductibility for ‘eligible capital assets’ like machinery, coffee machines and in my case office pinball machines (but excluding building and structural/ fit out costs).

This is great for those who made a profit last year, and can get back the tax they paid, if this years’ loss can soak it up. But the ‘loss carry back’ won’t continue next year.

For many of us though, claiming an immediate tax deduction on business stuff might not deliver the best financial outcome in the long term, given you also have the option of depreciating your asset pool by the usual 30% every year.

Dr. May was excited that the $300K she’s spent on dentist chairs for her surgery will be immediately tax deductible, meaning she won’t have to pay any tax at all for this year!

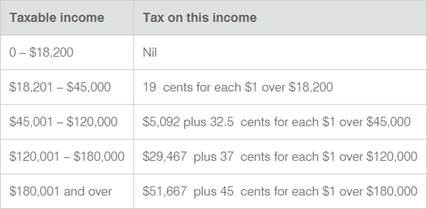

The problem is that this will by-pass this year’s (and future years’) smaller Marginal Tax rates that disappear every year. Use them or lose them. Below is how they’ll look:

By adopting Simplified Depreciation, she’ll have a tax bill this year, but will soak up the smaller MTR’s over the next 8 or so years, by consistently having smaller annual taxable incomes.

By spreading out the deduction over many years, she’ll only pay around $5K in tax on the first $45,000 every year, and be better off in the long-term.

It’s just one of those strange years. For many of us, going nuts at Officeworks next month might not be the best way. Personally, I’m holding off until July.

Back to my dentist client…

Dr May asked me to arrange a $300K unsecured equipment finance from Medfin, which she’d need to pay down over the next 5 years.

Bankers say that the term of a loan should reflect the life of the asset purchased. Hmm.

Whilst this can help with cash flow management for very big business, or will need be the case where the depreciating asset itself is the only collateral offered, there might otherwise be better ways.

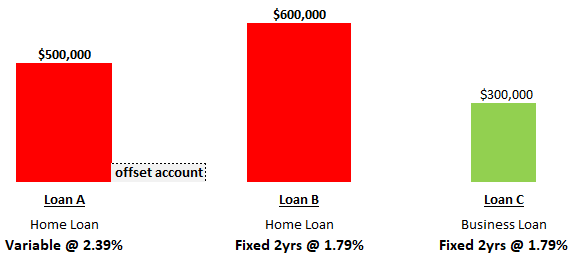

Dr May has ample equity in her newly acquired dream-home. We’re refinancing the loan to get it better structured, splitting the loan into variable and fixed splits as usual, but also setting up a 3rd $300K housing-loan-type-facility for her to use to buy the dentist chairs, for 2 good reasons:

1. The much cheaper rate of 79% per annum (the LVR is < 70%)

2. The 30-year loan term offered by this loan means she doesn’t need to pay this ‘good debt’ down quickly.

By stretching out deductible debt (green), Dr May has the ability to pay down her non-deductible home loans (red) faster. Well, adding to her offset balance to be more precise…

It’s for this very reason that we property investors consistently refinance our investment loans, re-setting the 30-year loan term every time.

A quick reminder for PAYG earners that even if you haven’t been salary sacrificing the last 10 months, new legislation allows you to now make a lump sum payment before June 30 and claim it in your 2021 tax return. Just remember:

1. The $25,000 cap includes what your employer has already paid, so if your salary is $100K + Super of 9.5%, you can only tip in an extra $15,500.

The extra $15,500 of concessional Super contributions will cop a 15% contribution tax, but if you’re on an effective tax rate of 39%, you pocket 24% of it, meaning you’re instantly $3,720 better off. Just like that.

$15,500 x (39%-15%) = $3,720

2. Just make sure you complete the ATO Notice of Intent to Claim for and send it to your superfund straight away (your accountant will help).

Whilst I grapple with the fact that I turn 51-years-old on Tuesday, I hope you’re all keeping well and have a lovely weekend,

Jason C. Khoury, JP, Financial Strategist, iChoice Managing Partner