Good day!

For those who will carry investment loans throughout the next financial year, you may be considering 3 options, depending on your goals and taxation strategy.

1. Principal & Interest

Keeping your loan P&I is generally preferred for those who already own their homes, or those who rent, and so don’t have any loans that they service with their after-tax dollars. For those who do have a home loan, they may still go P&I to enjoy the slightly cheaper interest rate, which can be fixed at 2.19%.

2. Interest-Only

Servicing investment loans on an interest-only basis costs slightly more these days but can still be fixed at 2.39%. It allows borrowers to concentrate on reducing their home loans faster.

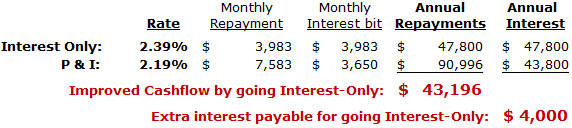

Dr Maria has a $2,000,000 investment loan she wants to refinance to get $3K cashback and fix for 2 years, so we presented both ways of doing it:

Dr Maria is happy to pay a little bit more in interest (to the tune of $4,000 per annum) so that she doesn’t need to pay down her investment loan. She actually owns her home, but might soon buy a holiday house, or non-concessionally contribute $200K into her SMSF. Either way, she may soon acquire some non-deductible debt so wants to go I.O. Good.

But Dr Maria then mentioned that in November, she made a $400,000 Capital Gain. This changes things!! $200,000 of this Capital Gain will be taxable at her marginal tax rate this financial year.

Her taxable income normally sits around $175K which is within the 39% tax bracket (including Medicare), but not a cent over. Same is expected for FY 2022.

But now, for 2021, Dr Maria will be smack in the 47% tax bracket, yuck…

3. Interest-In-Advance

…it’s the perfect time for Dr Maria to consider paying Interest-In-Advance for her $2M investment loan, where she’ll get 49% of the interest back as a tax deduction this July, rather than only 39% after the 2022 FY.

The I.I.A. rate is even cheaper than the standard I.O rate, given the bank gets their hands on your money earlier.

We’re lodging this now, applying for $2,045,000 to also cover the interest, to super-charge its effectiveness. The dominant purpose in her case is clear & within Part IV.

She’ll be nearly $5,000 better off by paying IIA in this year where she has an unusually high taxable income.

Paying I.I.A is often considered by people who might sit in a lower tax bracket next FY due to potentially losing their contract, about to retire or planning some extended time off to travel or have a baby.

Can I share something with you that’s highly embarrassing for a guy with a reputation of being a generous & charitable spender?

I paid for my fuel yesterday with my Woollies Rewards Card and the nice man swiped it saying, ‘you have a $10 credit, would you like to use it now?’ I said no.

Like I told Victoria in my office, my fuel is tax-deductible, so I’d rather wait and use my $10 credit when buying groceries, ‘why would I throw away $4.14?’

She responded, ‘get a life’. But secretly, I know she’ll do the same from now on 🙂

Bored? (GST 91c x 80% Vehicle Busines Use) + (Cost $9.09 x 80% x 47% MTR)

Wealth creation is about some big things, yes, but also about getting all the little things right. This includes saving a few grand a year on your mortgages, including locking part of your home loan away at 1.79%… yes, this is where my free service comes into play –

Your role to make people happier & healthier is I think the greatest speciality of all time, which is why I so love helping you guys. But making people happier & wealthier is also pretty cool, I love what I do.

When you’re good and ready, I’d like to see where you’re at and how I might be able to add some value. You don’t need to have a plan of attack, because like all of us, you don’t know what you don’t know, right? We’re all specialists.

Keep well, enjoy the sunshine,

Jason