Dr Penny & Bob live in their Sydney home, which for asset protection purposes was originally purchased 99% in Bob’s name. Good.

The building her surgery operates from is owned in both of their names. They knew this wasn’t ideal, but until I met with them in February, they had no idea that they could transfer this property into a Self-managed Superfund without the usual stamp duty payable, which on this $2M property would normally be a whopping $80,000!

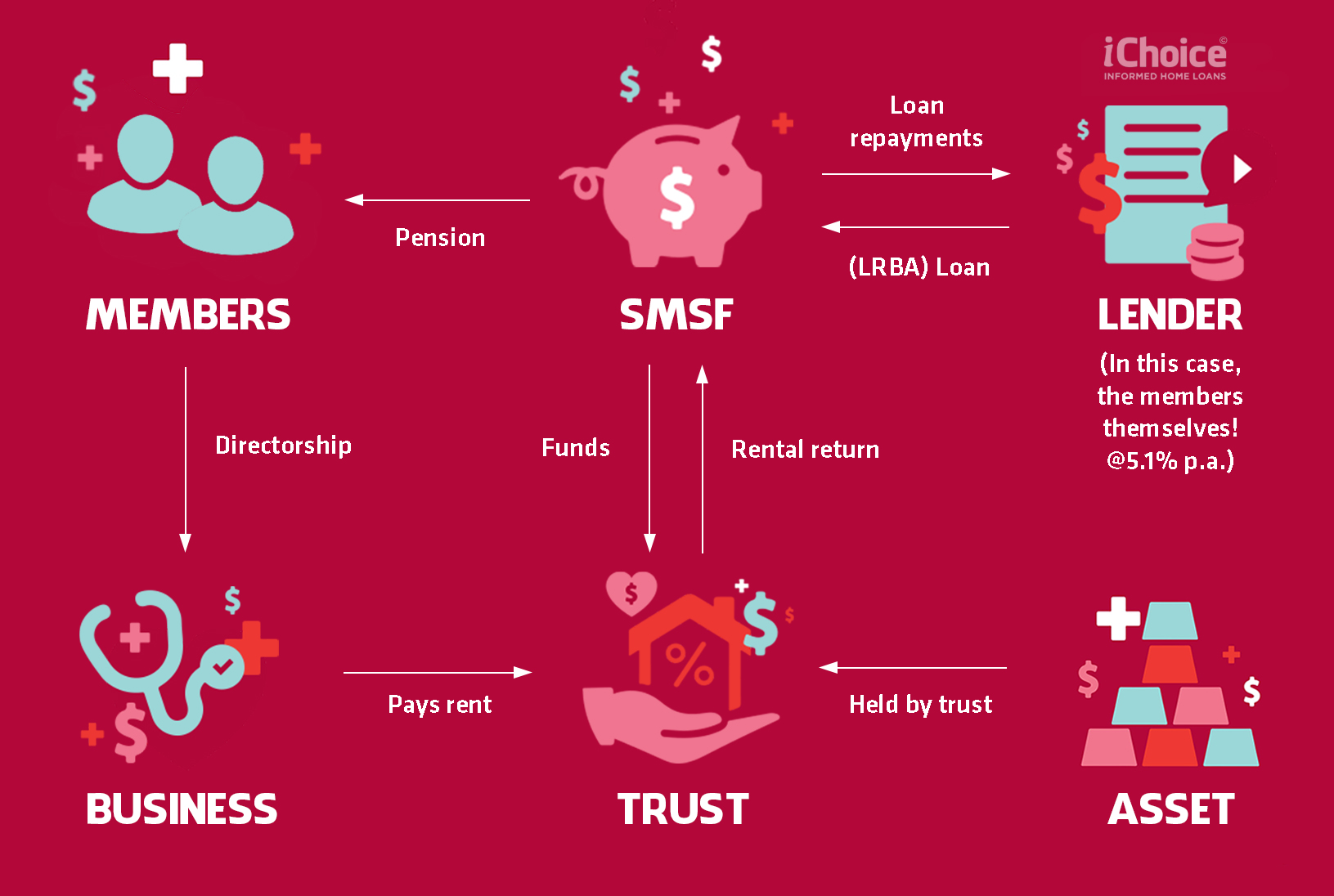

The best bit is that we’re leaving the dear commercial SMSF lenders completely out of the picture. This is how ~

Rather than the SMSF using a bank to borrow money, with my guidance, Penny and Bob have decided to be their own bank.

It’s not as complicated as it looks. Guys, let professionals do your heavy lifting, you just need to grasp the benefits, yes? Isn’t that what you’d say if I came to professionally see you?

So, how much does their SMSF need to borrow?

Well, they only have $500,000 in Super…not enough to come up with the $2,000,000 purchase price.

Their accountant will note a $330,000 non-concessional contribution into Super from each of them in FY 2023 at the time of the July settlement.

Non-concessional contributions are capped at $110,000 per annum. There is no tax deduction claimed for these contributions, but no 15% contributions tax either (obviously, since it has come from post-tax dollars).

People can use the ‘3-year bring forward rule’ to get $330,000 in (each).

Since the SMSF is buying the property off them, there is no need for this $660,000 to be physically transferred in Super; it’s rather just a swap. This amount can simply be deducted from the amount the SMSF needs to pay them. This is called ‘In Species’. No cash changes hands.

So, given they have $500K in Super already, and the $660,000 in species contributions, to acquire the property off them, the SMSF needs to borrow an extra $900,000.

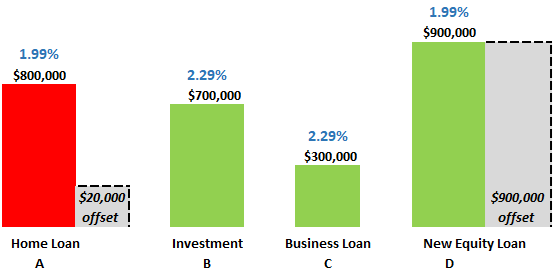

Just last week, we settled the refinance of their (A) home loan, (B) investment loan and (C) business loan, landing you-beaut rates & $6,000 in rebates. But more importantly, we created Loan D, a stand-alone $900,000 Equity Facility at 1.99% for them to use to on-lend to their SMSF.

This new Equity Facility has its own Equity offset account, so no interest will be charged on this loan until the funds will be actually used in July (that’s when these funds will be needed to lend to the SMSF so it can buy the surgery from them).

All their loans are tax-deductible (green) apart from their actual home loan which relates to their PPOR (red)

Now, get ready…

At the time of sale in July, Dr Penny & Bob will get the sales proceeds (less their contributions) of $900,000 which will come right back to them…

They can use this to extinguish their home loan! and still have another $120,000 to spend on whatever, including an overseas trip at the end of the year maybe, to celebrate all their loans now being green.

The Credit Card I arranged for them gives them free Qantas International Lounge passes, so go for it guys.

Do you see how they powerfully utilised the equity that built up in the surgery over the years to completely recycle all their debt into good debt?

And then, after July, the rent paid by the Practice will be taxed at 15% inside Super, which becomes 0% when they hang their boots up in 10 years. Beats marginal tax rates, wouldn’t you say?

It adds up to a gross tax saving of $632,000 over the next 20 years.

$80,000 x (47% – 15%) = $25,600 tax saving x 10 years = $256,000. The next 10 years: $80,000 x (47% – 0%) = $37,600 tax saving x 10 years = $376,000.

Their Land Tax will reduce by another $13,000 per annum. That’s another saving of $260,000 over the next 20 years.

Yep, SMSFs have their very own Land Tax Threshold. And you can have more than 1.

Show me the Money!

Sure, I haven’t accounted for the cost of having an SMSF set up, but also haven’t accounted for the compounding effect of the $892,000 saving, nor have I gone into the complex saving of how they will extinguish their home loan through debt recycling, where they have created good debt and extinguished bad debt.

Whilst a CGT event will officially take place, Small Business Tax Concessions should kick in to make it NIL.

SBTC will wipe out CGT tax as long as you haven’t used your $500K Lifetime Cap, and you pass the test; annual business turnover < $2M or have a Net Worth < $6M (excluding your home). You might be required to tip part into Super, but that’s OK, you need to anyway, right?

This is my boardroom in the iChoice building here in Sydney, safely tucked away for Tina and my retirement ~ to be more precise, it’s held in the name of iChoice Custodian Pty Ltd as Bare Trustee on behalf of Khoury Boys Pty Ltd ATF Khouryboys Superfund.

The poster on the wall was imported from Paris, an original vintage poster from the Moulin Rouge in 1976. iChoice bought it and claimed it as an immediate expense, but if I wanted to, our SMSF could have bought it. Yes, art can be purchased in Super.

Lucky I’d be able to display this poster in my office. Your Superfund’s collectable art cannot be displayed in your home; it must be wrapped up in paper and stored away…

SMSF’s provide amazing tax treatment to reward you solely for investing to fund your own retirement – NOT to give you any kind of personal joy.

Whether in Super or not, I’d really like self-employed people who are renting to consider buying commercial premises this year.

- If you’re bidding at an auction, you will have the edge over investors, who need to consider Tenancy Risk, management fees and vacancies

- If I’m your broker, you’ll likely be borrowing money at cheaper interest rates than others competing at the auction. You’ll be in front.

If NOT bought in Super, Suncorp Bank are waiving their establishment fee and charging 1.99% when residential security is being offered as collateral (otherwise it’s 2.49% with commercial collateral). Term can be 25 years. Same rate to go Interest Only 🙂

Sure, specialist lenders like Medfin and BOQ-S might fund 100% for Medics, but if that’s not necessary, let’s look at the cheaper options with longer terms

- Your business can perhaps claim a lot of the fit-out costs

Please consider allowing me to ‘fund’ the fit-out costs like in Loan C above that I did for Penny & Bob. It’s better than funding from cash flow or leasing stuff over the short term if you have the ‘Usable Equity’ to do so.

If bought in Super, the Lease your business has with your SMSF should really specify that ‘the tenant must remove all improvements made to the property by the tenant, at the end of the term’. Don’t leave yourself open to being accused of claiming stuff through your business that may have improved the value of the property.

- Having your own place will mean you don’t have a landlord who can boot you out but more importantly, having your own place just feels good. Personally, I have a lot of fun with it. Our office here feels like our second home.

- Residential property price growth is to cease for a bit; going commercial might be a better property investment

Whether an SMSF is on the cards or not, I’d love to speak with you about how tweaking your lending structure can benefit you and your family, even if we start at the beginning – with better interest rates and a couple of cash rebates.

Remember, for self-employed people without large undistributed company profits, I don’t need tax returns. Jut your last two NOA’s;

’20 & ’21 or for another few weeks, for ’19 & ’20.

That’s it! Such a game-changer.

The smartest thing I did 7 years ago was to channel my strengths and build this boutique, relationship-based, full-service brokerage. It was I guess my own internal ‘Mission Statement’ at the time…

…sorry, I watched Jerry Maguire with the kids last night, with the remote in my hand of course to forward through any raunchy scenes… hey, they’re 15, 13 and 11.

Thank you to all of you who are reaching out to me; I love my job, every day.

It completes me!

I wish you all a safe, lovely, and well-deserved Easter break 🙂

And upon your return, I’m on 0400 900 300 if you want to help me help you ~

Yours financially,

Jason