The Interest Rate Rise & The Looming End of the Financial Year

With the multiple interest rate rises recently, as you can imagine, there are many people getting in touch with us given the huge property-buying opportunities starting to pop up as well as reaching out to get a better rate as their banks pass on rate increases.

Last week’s rate rise of 0.5% was more than expected, and boy did it do some damage. The stock market cops it when rates rise, due to:

1. Equity investors assume company profits will drop given their customers (all of us) curb our spending a little, given our higher mortgage repayments

2. These big companies have a lot of debt themselves, so their bottom line will be affected directly by higher interest costs.

The only saving grace for the stock market is that some will stay well away from property for a while, and will have nowhere else to put their money. The ASX will quickly bounce back.

Rates still might not go as high as the market expects them to. The logic of the RBA mega-rise might have been to shock us into better spending habits, so we as a nation mightn’t need to endure the full brunt of too many rises.

But there’s another 0.5% rise looming, just around the corner, so get ready.

Many are structuring their lending to get ready to buy something, whether it be soon or next year. This is now a buyers’ market and bargains will be enjoyed by some.

Here’s 3 tips if you want to be one of them:

1. People don’t attend 3 auctions and get 3rd time lucky. They go to 20 auctions to find their bargain. I know it can be tiring to attend all these auctions in the hope that you’ll get lucky – but maybe you need to change your mindset.

Be prepared and go on little Saturday day trips, try the local cafés, make it like your little Saturday sport!

Like I tell my kids, the harder you work, the luckier you’ll get.

2. Try to find out whether the vendors are committed elsewhere, so you’ll be sure you’re not wasting your time and that the place will actually be sold on the day. Here’s a free tip…

… when searching in RealEstate.com or Domain.com, filter a keyword to be ‘motivated’. Agents only really put that in the ad if the vendors really are.

PS don’t feel bad about that. The market is the market. ‘Motivated’ vendors going to auction will be happy for you to turn up!

3. Get an Equity facility arranged against your home loan, as big as it can be with its own offset account. This might mean ‘reducing’ the home loan.

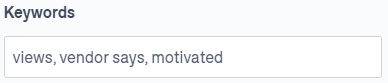

Consider Johnny who came to me last month with a $1.3M home loan with $500,000 in his offset. He understood that his (what we at iChoice call) ‘effective balance’ is only $800,000 – but he likes having half a mill lying around for a rainy day, cool.

But it’s smarter for him to have his unlocked equity separate to his home loan. Otherwise, by pulling money out of his home loan, he’s kinda increasing his non-deductible home loan (the nasty one that you need to service from your after tax dollars).

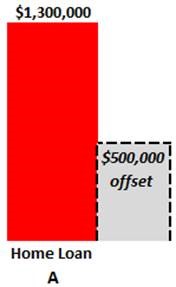

So we restructured his lending to leave his Unlocked Equity in a brand new ‘Loan B’, increasing it a bit at the same time ~ why not.

He plans on lending $200,000 to his SMSF soon to repay a nasty expensive loan he’s had for ages, so sorry to make things complicated, but we established ‘Loan C’, with it’s own offset, so this facility was also separately identifiable.

Loan A reflects his effective debt relating to his home and no more, other than the $10,000 in his transactional offset

It’s couloured red, as the interest on this loan is not tax deductible. This is the loan he needs to concentrate on paying down first, and fast.

Loan B reflects the unlocked equity; it’s all in the Equity offset account, so no interest is payable on this loan. It’s essentially a Line of Credit, just upside down, and cheaper.

It’s coloured amber, as the tax deductibility of this split will be subject to what purpose he actually uses the funds for on this newly established facility. If he buys shares with it, it will become green.

Loan C is his new facility ear-marked to be on-lent to his SMSF, so it’s green (tax deductible)

It’s fantastic that banks offer you $4,000 to refinance to them, and getting new-to-bank rates certainly doesn’t hurt these days, but really getting stuff structured right, and getting the best advise along the way, can make all the difference.

Even your beauty rates don’t sound that good these days anyway. The old 1.94% available 2 months ago has now gone up by 0.25% and yesterday another 0.50%, so is now 2.69%!

If it makes you feel any better, most borrowers will look at their home loan statement next week and see that it starts with a 3!

Personally, my intention is to get a really nice holiday house. Funny how one’s investment strategies change at age 52…

I’m quite sure that a combination of our big bad cities finally re-opening up after Covid, and with the heat now taken out of property prices, many of those who sought a sea-change or a tree-change the last few years might miss their social networks and be drawn back to the big smoke.

But given Tina and I have exceeded out Land Tax Thresholds and the fact that we want to buy here in NSW, to avoid Land Tax we’ll need to wait till January 2025 (or buy a farm, but I’m too old for that stuff).

Gotta play within the rules! Also helps if you know them all, though, right?

For those looking to improve their Capacity so we can actually approve the biggest loan for you, have a think before you complete your 2022 tax return in a few weeks.

I explained to a couple yesterday that we don’t need their company or individual tax returns these days, and can rather simply work off their Notices of Assessments (game-changer btw).

For that reason, they will be depreciating the Mercedes they just bought over 5 years, rather than writing it off immediately.

For the rest of us, trying to beef up our 2022 tax return helps best if we seek our pre-approval from a bank that looks at 2022 in isolation (a few do)…

…don’t worry about getting your tax deductions a little earlier; if you’re anything like me, you’ll be buying those things at Officeworks in July, not June.

I’m here to help in any way I can guys, on 0400 900 300. You know what they say… if you want something done right, ask someone busy ~

Yours financially,

Jason