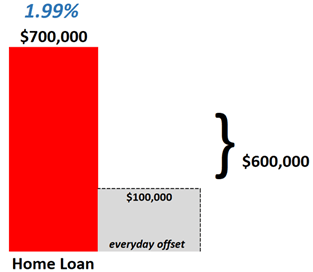

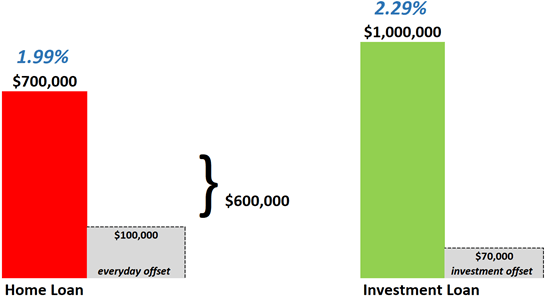

Jack and Jill had a $600,000 home loan at some weird lender who offered a good rate a few years ago but has since turned into a dud. They asked me to refinance their loan to a big 4 bank. Good.

They also wanted to have an extra $100,000 ready to build a pool in the backyard at some point, maybe next year. But they didn’t want any more than that.

They weren’t interested that much in a cash rebate, stating they were more interested in the long-term benefit and left it to me to come up with my best recommendation.

We ended up refinancing their home loan to a packaged product with a lifetime discount resulting in a rate of 1.99%, and a $3,000 cash rebate on top, just for fun.

We increased the loan amount so they could have the $100,000 sitting in their offset account, which they can access when they’re good and ready.

My awesome Team!

The extra $100,000 is now sitting in their offset account and until they actually use it, they’re only paying interest on the ‘effective balance’ of $600,000.

I also refinanced their $1M investment loan which was at a high rate of 3.1% at the Commonwealth Bank. We could arrange a much better investment rate of 2.29%, as long as it was P&I.

Oh so sorry guys, another $3,000 refinance rebate again, gee I don’t listen, sorry! But the lower rate will save you $8,100 a year also so don’t get to cranky-pants on me ~

But Jack was not happy!

His brother-in-law is an accountant, so he’s been taught that he should preserve the capital of his ‘good’ deductible investment loan – and choose to go interest-only, allowing them to more quickly pay down their ‘bad’ home loan (which relates to their PPOR and is serviced with their after-tax dollars). Hmm. He’s kinda right ~

Jill was happy to go P&I, when I explained that to go Interest-Only for 3 years, the rate would be 2.49% (a bit higher).

Until 6 years ago, it was an easy decision to choose Interest-Only for investment loans, given there wasn’t a premium slapped on the rate to do so! And back then, us in Financial Services were a little irresponsible; we were still calculating Capacity over a notional 30-year-loan term, rather than the actual remaining P&I term they’d end up with once the I.O period finishes. Some banks were fined millions of dollars for doing this.

If Jim got his way, the annual repayments of Interest Only on their $1M investment loan would be kept to $24,900 per annum. Over 3 years this is $74,700.

Interest only on $1M x 2.49% = $24,900 x 3 years = $74,700

If Jill got her way and went P&I, the rate of 2.29% (20 basis points cheaper) will save them around $2,000 per year in interest, so $6,000 over 3 years.

BUT, the P&I loan would require them to also make principal reductions over the 3 years to the tune of around $70K.

So, the decision they had to make was whether they should be OK to reduce the balance of their investment loan (rather than their home loan) by $70,000 – to be better of by $6,000. It’s a tough one.

It’s a matter of tax strategy Vs interest saving. For the 99% of people who are happy to pay much more than 2.49% to go I.O, this calculation is much more severe, where the ‘interest cost’ of going IO is much higher.

In the end, the most important thing to Jack & Jill was their ability to buy another investment property, so we went P&I on their investment loan.

When calculating their maximum pre-approval, I load into the banks’ calculator the P&I repayment over a 30-year loan-term, rather than over the shorter period of 25 years if they went I.O (being the P&I term they would have had, once their I.O period finished).

Let me complicate things a bit, now (as I do)…

When we refinanced their $1M investment loan, we actually increased the limit by $70,000; these extra funds are now sitting in their investment offset account. Hmm, I hear you say.

How you can legally capitalise investment interest is something I’ll leave alone for now. If your accountant and yourself can get your heads around the clear-as-mud tax ruling in TR 98/22 I congratulate you.

In fact, if you can get 5 accountants to agree amongst themselves, I’ll also congratulate you.

Bit it’s something that’s quite commonplace when people pay Interest-In-Advance. Like what I’m doing for Dr Cathy…

Cath made a Capital Gain in November which puts her way into the top marginal tax bracket. It’s a smart move for her to pay the interest for her $2M investment loan for the 2022/2023 FY, this side of July 1.

Claiming the $50K interest deduction this FY at 45 cents makes more SENSE than claiming it when back on the 37 cent–bracket next FY. It’ll save her around $3,200.

$40,000 x (0.45-0.37) = $3,200

I hears ya, is it even worth it? Just for $3,200 and a $3K rebate? Well, it took Cathy about 3 hours in total to get me a few things and pop into the branch to sign some docs. She knows that nobody else is going to pay her $2,000 per hour for her time so with both hands she took the advice and grabbed the opportunity. Good, getting ahead faster comprises of a bunch of little things, I say.

Alas, I digress,

We’re applying for $2,050,000 for Dr Cathy, to cover the interest also. We need to because we’re paying the interest-in-advance, right?

My point? Surely this is capitalising interest?! To me, it looks like interest-only on steroids!

I hope you found something interesting in all that. Now, a tiny sales pitch if you could gracely allow me:

Guys, if you have total lending over $1M, and your loans are less than 70% of the value of the security properties, please give me and my team a go. These big 4 bank rates aren’t published, don’t bother trying to google them.

Lending > $1M and < 70% LVR, lifetime packaged discounts result in:

Home Loans: 1.99%

Equity Loans: 1.99%

Investment Loans: 2.29%

Investment Loans Interest-Only 2.49%

Commercial Loans: 2.29% [if secured by reidential property]

A refinance isn’t just about a better rate and a $6,000 rebate-grab, remember. It can be a chance to consider strategy, and restructure;

Can we shuffle securities around with updated valuations, or even release one of your properties to keep it liquid?

Is there any investment or business expenses coming up, that we should prepare a separate split for?

Every time you refinance, your Capacity is improved, given the reduced minimum-mandatory repayments, given the fresh 30-year-loan term

Hold up! It’s not about stretching the loan itself to 30-years, of course, you’ll pay it down as fast as you can. It’s just about reducing your contracted & minimum required monthly repayments – that’s all the banks are interested in when seeing how much more you can borrow

Is it time to get a pre-approval in place? They’re free to get and normally last 6-months. When rates start to rise, and they will, so will some great buying opportunities. Be prepared ~

Don’t think that refinancing and restructuring necessarily mean you need to change the way you do all your banking. I have 14 bank accounts at the CBA and I’ll never change that; I’m too addicted to Netbank. But my lending will sit with their competitors who right now are helping me and my family get ahead the fastest, sorry.

I’m supported by the cleverest bunch of mortgage professionals in the country – and right now we’re on fire. I’m on 0400 900 300 if you’d like to be part of it and give us a crack ~

Otherwise, hang in there, keep cool, have a top weekend,

Yours financially,

Jason